The financial sector has moved past the “proof of concept” phase. In 2026, the implementation of AI in finance is no longer a luxury for innovation labs; it is a fundamental requirement for institutional survival. As markets become more volatile and data volumes reach petabyte scales, the human capacity for manual analysis has hit a hard ceiling.

According to recent data from the Financial Stability Board and McKinsey, AI in banking and finance is projected to deliver up to in $1 trillion additional value annually. This massive shift is driven by a move away from simple chatbots toward autonomous, agentic systems that can reason through complex regulatory and fiscal data. As we cross this threshold, the industry is witnessing a divergence between the “Tinkerers” firms still stuck in limited pilots, and the “Integrators” organizations that have re-architected their core processes to be human-led and AI-operated.

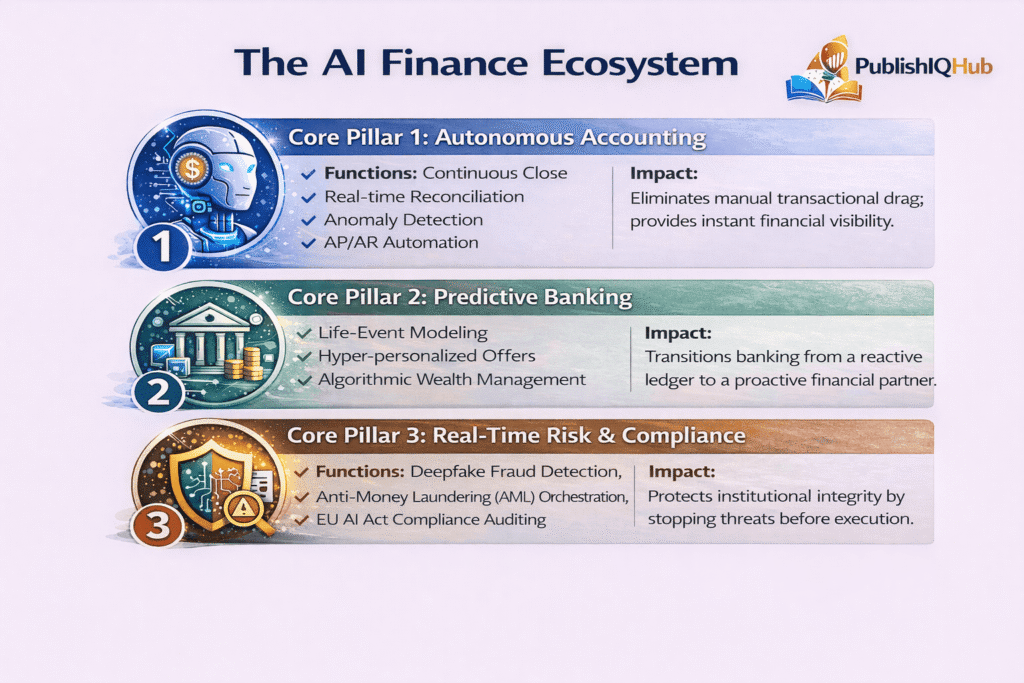

The New Architecture: AI for Financial Services

To understand why this shift is happening, we have to look at AI for financial services through three distinct functional lenses. This is the “What” of the modern financial stack.

1. Predictive Banking and Personalization

In AI in banking and finance, the goal has shifted from transaction processing to “Life-Event Prediction.” Modern AI doesn’t just categorize your spending; it analyzes temporal patterns to predict a customer’s need for a mortgage, a car loan, or a wealth management pivot months before the customer even realizes it. By shifting from reactive service to proactive partnership, banks are seeing a 30% increase in Customer Lifetime Value (CLV).

2. The Autonomous Back Office

This is the “What” of AI in finance and accounting. The traditional “Month-End Close” is being replaced by a “Continuous Close.” AI agents now operate across ERP systems to:

- Auto-Match Records: Identifying and reconciling intercompany transactions in real-time.

- Flag Strategic Variance: Moving beyond simple budget tracking to explain why a department is overspending based on external market data.

- Predict Cash Flow: Using historical payment behaviors of specific vendors to provide a 90-day cash forecast with 98% accuracy.

3. Real-Time Risk and Fraud Orchestration

Traditional fraud detection was a game of “catch-up.” Today, AI models reason across global geopolitical events, social sentiment, and transaction metadata to identify high-risk anomalies before the money leaves the account. In a world of deepfakes and sophisticated cyber-attacks, this layer is the only thing protecting institutional integrity.

Leading the Charge: 15 Top AI in Finance Providers

The market is rapidly consolidating around specialized players who understand the “guardrails” required for financial data. Here are fifteen providers currently defining the state of the art:

- Bloomberg (BloombergGPT): The gold standard for domain-specific LLMs, trained on decades of financial data to provide unparalleled market sentiment analysis.

- BlackLine: The leader in accounting automation, specifically for the “Continuous Close” and automated reconciliation.

- HighRadius: An AI-powered platform for Order-to-Cash and Treasury, focusing on reducing Days Sales Outstanding (DSO) for enterprises.

- Kyriba: Leveraging AI for global liquidity management, helping CFOs see and move cash across thousands of bank accounts instantly.

- Workday Adaptive Planning: Using machine learning to drive the “FP&A of the future,” where every budget is a living, breathing forecast.

- Upstart: A pioneer in AI-driven lending, using non-traditional data points to provide more accurate credit assessments than FICO alone.

- Zest AI: Specifically built for credit unions and banks to automate underwriting while ensuring compliance with fair-lending laws.

- Kasisto: Providing the most advanced conversational AI for banking, capable of handling complex financial inquiries that generic bots fail on.

- Vena Solutions: Integrating AI directly into the Excel-based workflows that finance teams already use, making the transition to AI frictionless.

- DataRobot: An enterprise AI platform that allows banks to build, deploy, and manage their own proprietary risk and fraud models.

- Anaplan: Driving connected planning across the enterprise, using AI to align finance, sales, and supply chain data in one view.

- Tipalti: A leader in Global Payables automation, using AI to manage the entire “Procure-to-Pay” cycle across multiple tax jurisdictions.

- Ocrolus: Specialized in document AI, extracting data from tax returns and bank statements with human-level accuracy for faster mortgage processing.

- Feedzai: The world’s first “RiskOps” platform, using AI to combat financial crime and money laundering in real-time.

- Bill.com: Transforming SMB finance by using AI to automate the accounts payable and receivable process for millions of small businesses.

The Implementation Gap: Why Infrastructure is the Real Moat

The “How” of AI in finance is where most firms fail. Success is not about buying the best model; it is about building the right infrastructure to feed that model.

The Move to “Data Intelligence Platforms”

Traditional data warehouses are too slow for the agentic era. High-growth firms are moving toward “Lakehouse” architectures that allow AI to reason across unstructured data (like PDF contracts and earnings call transcripts) and structured data (like ledger entries) simultaneously. Without this unified view, your AI is essentially working with one eye closed.

Governance as a Feature, Not a Bug

In the financial sector, a “black box” is a liability. The most successful AI implementations in 2026 are those that prioritize Explainability. Every decision made by an AI agent, whether it’s a loan denial or a suspicious activity flag, must come with a clear audit trail. This isn’t just for the regulators; it’s for the trust of the customers.

Scaling Your Strategy: A Step-by-Step Blueprint

How do you take a legacy finance department and turn it into an AI-powered growth engine? It

requires a staged approach:

Step 1: The “Manual Debt” Audit. Identify the processes where your highly-paid analysts are spending more than 40% of their time on data entry or formatting. These are your first targets for automation.

Step 2: Pilot “Side-by-Side” Agents. Introduce AI agents as “co-pilots” for your team. Let the AI handle the data preparation and outlier detection, while the human handles the final interpretation and approval.

Step 3: Normalize the “Data Spine.” Standardize your definitions across departments. If “Revenue” means something different to Sales than it does to Finance, your AI will produce conflicting insights.

Step 4: Real-Time Strategic Activation. Shift your team’s focus from “What happened last month?” to “What is happening right now, and what will happen next month?” This is where finance becomes a strategic leader in the boardroom.

Conclusion: Moving From Hindsight to Foresight

The shift toward AI in finance is fundamentally a shift in perspective. Historically, finance has been the department of “hindsight”- measuring what has already occurred. In the era of agentic intelligence, finance becomes the department of “foresight.”

By prioritizing infrastructure over hype and focusing on the “Why What and How” of implementation, you are doing more than just cutting costs. You are building an organization that can move as fast as the market demands. The divide between the “tinkerers” and the “integrators” is widening by the day. The only question left is where your institution will stand.

The shift toward precision is happening now. Follow along with our weekly deep dives to make sure your organization stays on the right side of the digital divide.

Frequently Asked Questions

Is AI too risky for regulated banking?

No, but it requires a “Human-in-the-Loop” architecture. The goal isn’t to let the AI make final decisions autonomously; it’s to have the AI provide the best possible data and options for a human expert to review.

How do we handle the “Hallucination” problem in accounting?

By using RAG (Retrieval-Augmented Generation). Instead of letting the AI guess based on its training data, RAG forces the AI to look at your specific, verified internal documents (the “Golden Records”) to find the answer.

What is the biggest barrier to ROI in AI finance?

Legacy systems. AI agents are only as fast as the APIs they can talk to. If your core banking or ERP system is 20 years old and doesn’t support modern integrations, your AI will be throttled.

Does the “Agentic Era” mean we need fewer people?

It means you need different skills. You need fewer data entry clerks and more “AI Orchestrators”- people who can design workflows, manage AI performance, and interpret complex outputs.