Disclaimer: The content in this blog is for informational and educational purposes only

and does not constitute investment advice, stock recommendations, or a solicitation to

buy or sell any securities.

The problem with most financial advice is that it treats you like a calculator rather than a human being. We are told to “buy low and sell high” as if our emotions don’t scream the exact opposite when the markets actually dip.

Finding the best mutual fund to invest now isn’t just about scanning a spreadsheet for the highest percentage; it’s about finding a strategy that aligns with your personality, your goals, and your actual tolerance for risk when things get messy.

This guide is designed to peel back the curtain on the top mutual fund companies in India. We aren’t just looking at who has the most money under management; we are looking at their “institutional soul”- the specific investment philosophies that dictate how they handle your money.

Whether you’re a first-time investor looking for a good mutual fund to invest in for the long haul or a seasoned pro trying to optimize for the 2026 tax laws, you need a roadmap that balances technical precision with human reality.

The Institutional Vanguard: A Deep Dive into the Top 15 Mutual Fund Companies

Backing a mutual fund is essentially backing an investment philosophy. The following profiles examine the 15 titans of the Indian AMC world, detailing their strategic moats and why they remain the preferred choice for millions of portfolios. As of April 2026, the industry is dominated by five giants, each with a distinct strategic moat and a total industry AUM standing at ₹73.73 Lakh Crore.

| Mutual Fund Company (AMC) | AUM (Scale) | Investment Philosophy | Key Strength (Moat) | Best Suited For |

| SBI Mutual Fund | ₹12.8 Lakh Cr+ | Conservative, diversified | Strong PSU-backed trust + distribution reach | Conservative investors |

| ICICI Prudential Mutual Fund | ₹11.7 Lakh Cr+ | Dynamic, counter-cyclical | Expertise in hybrid & multi-asset allocation | Tactical allocation |

| HDFC Mutual Fund | ₹9.5 Lakh Cr+ | Long-term, quality-focused | Strong credit discipline & blue-chip exposure | Wealth creation |

| Nippon India Mutual Fund | ₹7.5 Lakh Cr+ | Aggressive + passive blend | ETF leadership + small-cap alpha | Passive + high growth |

| Kotak Mahindra Mutual Fund | ₹5.5 Lakh Cr+ | Risk-managed investing | Liquidity-first “SLR” framework | Moderate risk investors |

| Aditya Birla Sun Life MF | ₹3.9 Lakh Cr+ | Thematic & sector-focused | Strong in infra & manufacturing themes | Sector bets |

| UTI Mutual Fund | ₹3.5 Lakh Cr+ | Value-driven, research-based | Legacy + bottom-up stock picking | Value investors |

| Axis Mutual Fund | ₹3.2 Lakh Cr+ | Quality growth | Focus on clean balance sheets | Premium growth |

| DSP Mutual Fund | ₹2.1 Lakh Cr+ | Rule-based, systematic | Data-driven investing approach | Disciplined investors |

| Mirae Asset Mutual Fund | ₹2.1 Lakh Cr+ | Growth-oriented | Strong mid-cap & emerging leaders focus | Mid-cap exposure |

| Tata Mutual Fund | ₹2.0 Lakh Cr+ | Ethical, governance-led | ESG-oriented investing philosophy | Ethical investors |

| Bandhan Mutual Fund | ₹1.8 Lakh Cr+ | Active debt strategies | Dynamic bond management expertise | Income stability |

| Edelweiss Mutual Fund | ₹1.8 Lakh Cr+ | Passive + debt innovation | Target maturity & index debt funds | Debt diversification |

| PPFAS Mutual Fund | ₹1.4 Lakh Cr+ | Value + global investing | Skin-in-the-game philosophy | International diversification |

| Motilal Oswal Mutual Fund | ₹1.3 Lakh Cr+ | High-conviction investing | Concentrated “Buy Right, Sit Tight” approach | Aggressive investors |

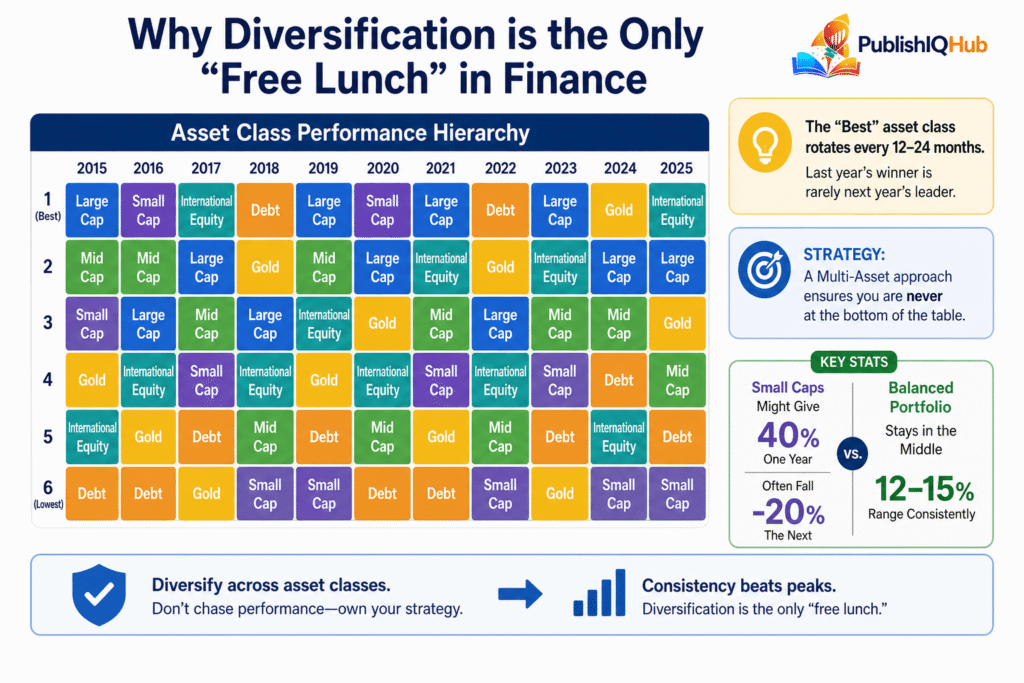

Deciphering the Best Mutual Fund to Invest Now: Sectoral and Cycle Logic

Identifying the best mutual fund to invest now requires more than a cursory look at the 1-year return. It requires an understanding of the current market “Regime.” In a late-cycle bull market, “Quality” and “Stability” become more important than “Growth.”

The Flexi-Cap Dominance

For 90% of investors, the “Best Now” answer is a high-quality Flexi-Cap Fund. Unlike sectoral or small-cap funds, a Flexi-Cap gives the fund manager the power to move into Large-caps when the market is expensive and pivot to Mid-caps when valuations drop.

HDFC Flexi Cap and Parag Parikh Flexi Cap are current favorites because of their ability to hold cash or move into international stocks when Indian valuations feel stretched.

The Rise of Multi-Asset Allocation

In a world where interest rates are volatile and gold is hitting new highs, “Multi-Asset Funds” have emerged as the ultimate “all-weather” investment. By holding Equity, Debt, and Gold in a single scheme, these funds provide a built-in rebalancing mechanism that protects you from a crash in any single asset class.

The Technical Filter: Beyond the Star Ratings

When sophisticated investors look for top mutual funds to invest in, they ignore the “stars” and look at the “guts” of the fund. Here is the quantitative checklist you should use:

1. Downside Capture Ratio (DCR)

This is the most critical metric for wealth preservation. If the Nifty falls by 10% and your fund only falls by 7%, it has a DCR of 70. A good mutual fund to invest in should ideally have a DCR below 85. This ensures that when the market “sneezes,” your portfolio doesn’t catch a “cold.”

2. The Sortino Ratio

Standard deviation (used in the Sharpe Ratio) penalizes all volatility-even the “good” volatility (upward spikes). The Sortino Ratio, however, only penalizes “bad” or “downside” volatility. A higher Sortino ratio indicates that the fund manager is delivering returns without making you lose sleep over massive drops.

3. Active Share

If you are paying for an active fund, you want the manager to actually be active. “Active Share” measures how much the fund’s portfolio differs from its benchmark. If the Active Share is below 60%, you are paying “active” fees for a “passive” index-like return. This is known as “Closet Indexing,” and it is a major wealth-killer.

The “Nurture Bridge”: The Psychological Barrier to Wealth

The term “Nurture Bridge” refers to the period between your initial investment and the realization of your financial goal. This is where most investors fail-not because of bad funds, but because of bad behavior.

The Psychology of Loss Aversion

Studies in behavioral finance show that the pain of losing ₹10,000 is twice as intense as the joy of gaining ₹10,000. This “Loss Aversion” causes investors to panic-sell during temporary market corrections, effectively locking in their losses.

The top mutual fund companies build their frameworks to manage this by offering “Systematic Withdrawal Plans” (SWP) and “Systematic Transfer Plans” (STP) to automate discipline.

The Cost of Delay

One of the most misunderstood concepts in investing is the “opportunity cost” of waiting for a market correction. Data shows that “Time in the Market” is far more powerful than “Timing the Market.” Waiting just 12 months to start a ₹10,000 SIP can result in a loss of several lakhs in your final 20-year corpus.

The Regulatory Revolution: Why Transparency is Winning

Following the landmark regulatory updates, the focus of the top mutual fund companies has shifted toward “True-to-Label” mandates.

TER Revisions

The Total Expense Ratio (TER) is no longer a hidden cost. AMCs are now required to break down exactly how much is going toward fund management, marketing, and brokerage. This has led to a “Price War,” significantly benefiting the retail investor.

Portfolio Overlap Disclosures

One of the biggest issues for retail investors is holding three different funds that all own the same 20 stocks. The new “Portfolio Overlap” disclosure norms force AMCs to show exactly how much their various schemes mimic each other. This transparency allows you to pick top mutual funds to invest in that truly diversify your holdings rather than just duplicating them.

The Exit Architecture: Master the Art of the “Smart Withdrawal”

The most dangerous phase of investing isn’t the beginning; it’s the end. If you have spent 15 years identifying the best mutual fund to invest now and building a massive corpus, you cannot afford to let a single bad year or a poor tax strategy ruin your “Closed-Won” financial status. Sophisticated wealth management requires an exit strategy that is as disciplined as your entry.

1. The Three-Year “Glide Path” Strategy

You should never sell your entire equity portfolio on the day you need the money. Instead, implement a “Glide Path” starting 36 months before your goal date.

• The Process: Gradually move your profits from high-alpha equity funds into ultra-safe Liquid Funds or Arbitrage Funds from the top mutual fund companies.

• The Benefit: This protects your goal from a “Black Swan” event (like a sudden market crash) right when you need the cash. It ensures that your child’s education or your retirement home is funded by “locked-in” gains rather than “paper profits.”

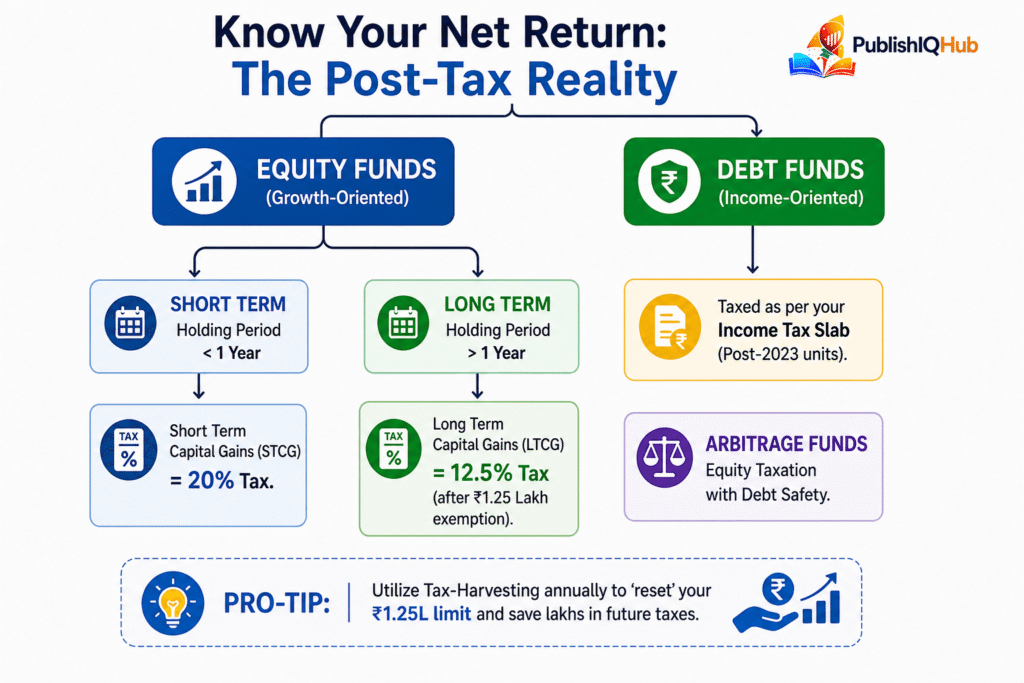

2. Mastering the Systematic Withdrawal Plan (SWP)

In 2026, the SWP has become the preferred tool for generating a “DIY Salary.” Instead of taking a lump sum, you instruct the AMC to redeem a fixed amount every month.

• Tax Efficiency: Unlike traditional dividends (which are taxed at your income slab), an SWP is treated as a partial redemption of capital and capital gains. Only the “profit” portion of your withdrawal is taxed, and if held for over a year, it falls under the lower 12.5% LTCG bracket.

• Rupee Cost De-Averaging: Much like an SIP helps you buy more units when prices are low, an SWP ensures you sell fewer units when the market is down, preserving your capital for longer.

3. The “Tax Harvesting” Annual Reset

One of the most powerful “Nurture Bridge” activities is the annual reset of your cost basis.

• The 1.25L Strategy: Every financial year, you are allowed ₹1.25 Lakh of Long-Term Capital Gains (LTCG) tax-free.

• The Play: Even if you don’t need the money, you should sell units to book a profit of ₹1.25 Lakh and immediately reinvest the proceeds into a good mutual fund to invest. This “steps up” your purchase price, significantly reducing the massive tax bill you would otherwise face 10 years down the line.

4. Avoiding the “All-or-Nothing” Exit Trap

Many investors panic-sell their entire portfolio when they see a 10% dip. In the 2026 market, volatility is a feature, not a bug.

• The Diagnostic Check: Before exiting a fund, check its Relative Strength Index (RSI). If the fund is underperforming because its entire sector (e.g., IT or Pharma) is down, don’t sell. If it is underperforming while its peers are rising, that is a signal that the top mutual fund company managing that scheme has lost its way, and it’s time to pivot.

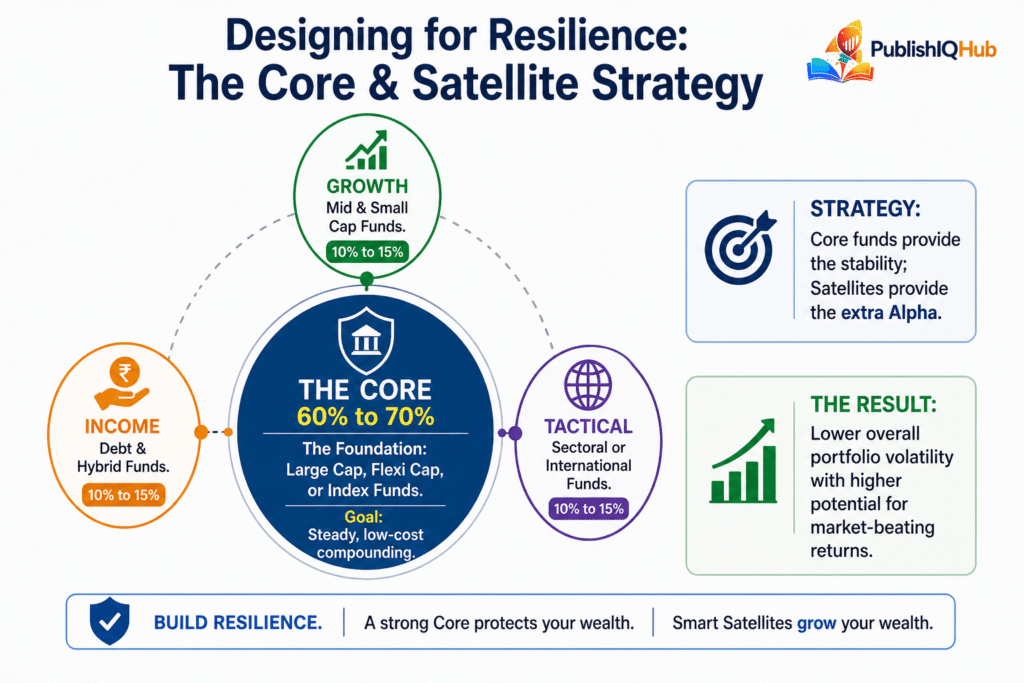

The Final Verdict: Engineering Your Legacy

Building a portfolio across the top mutual fund companies is about more than just numbers on a screen; it’s about engineering the freedom to walk away from a job you don’t like or fund a dream you’ve deferred. By focusing on “Institutional DNA,” leveraging the Core-and-Satellite model, and mastering the Exit Architecture, you aren’t just “saving”-you are operating a sophisticated financial machine.

As we move deeper into 2026, the gap between the “average” investor and the “informed” investor will continue to widen. The tools are now in your hands. To stay updated on the latest True-to-Label regulatory changes, keep reading our blog and stay committed to the compounding journey.

Frequently Asked Questions

1. What is the best mutual fund to invest now for a 10-year retirement goal?

A combination of a Flexi-Cap Fund (for core stability) and a Mid-Cap Fund (for growth) is generally the most effective strategy. This duo balances the safety of large businesses with the explosive growth of mid-market leaders.

2. Which top mutual fund companies are best for NRI (Non-Resident Indian) investors?

SBI, ICICI, and HDFC have the most robust digital onboarding and compliance frameworks for NRIs, particularly those residing in the USA or Canada who face stricter FATCA/CRS reporting requirements.

3. Are Index Funds better than Active Funds in the current market?

In the Large-Cap category, Index Funds are often superior because they have much lower costs and most active managers struggle to beat the Nifty 50 consistently. However, in the Mid and Small-Cap spaces, active managers can still find “hidden gems,” making active funds a better bet there.

4. Can I still get 15% returns in the current economy?

While historical returns have been high, a realistic expectation for a diversified portfolio across the top mutual fund companies is 12% to 14% CAGR over a long horizon. Chasing 20% often leads to excessive risk-taking.

5. How do I switch from a Regular Plan to a Direct Plan?

You can do this through the AMC’s website or apps like MF Utility. However, remember that a “Switch” is treated as a “Redemption” for tax purposes. If you have been in the fund for less than a year, you may be liable for STCG tax.