The global financial landscape has shifted from traditional brick-and-mortar institutions to a highly integrated, software-driven ecosystem. Now, the distinction between a technology company and a financial institution has largely vanished.

As digital payments, embedded lending, and real-time cross-border transfers become the standard, businesses and consumers are looking for the most reliable partners to manage their capital.

This transformation is not merely about moving bank accounts to an app. It represents a fundamental restructuring of how value is moved across borders and how credit is assessed. Traditional banks are increasingly finding themselves acting as the back-end utility, while the leading fintech companies own the customer relationship, the user experience, and the data insights.

Identifying the top fintech companies is no longer just about finding a place to store money; it is about selecting a strategic partner that offers the best integration, the highest security, and the most transparent fee structures.

Why Modern Enterprises are Partnering with Leading Fintech Companies

The primary driver of fintech’s explosive growth is demand for speed, transparency, and interoperability. Traditional banking systems, often built on legacy mainframe infrastructure from the 1980s and 90s, struggle to keep pace with the real-time demands of the modern economy. In contrast, leading fintech companies operate on cloud-native platforms that allow for near-instantaneous processing and deep data insights.

For companies looking to scale globally, the best fintech startups and established leaders offer three distinct competitive advantages:

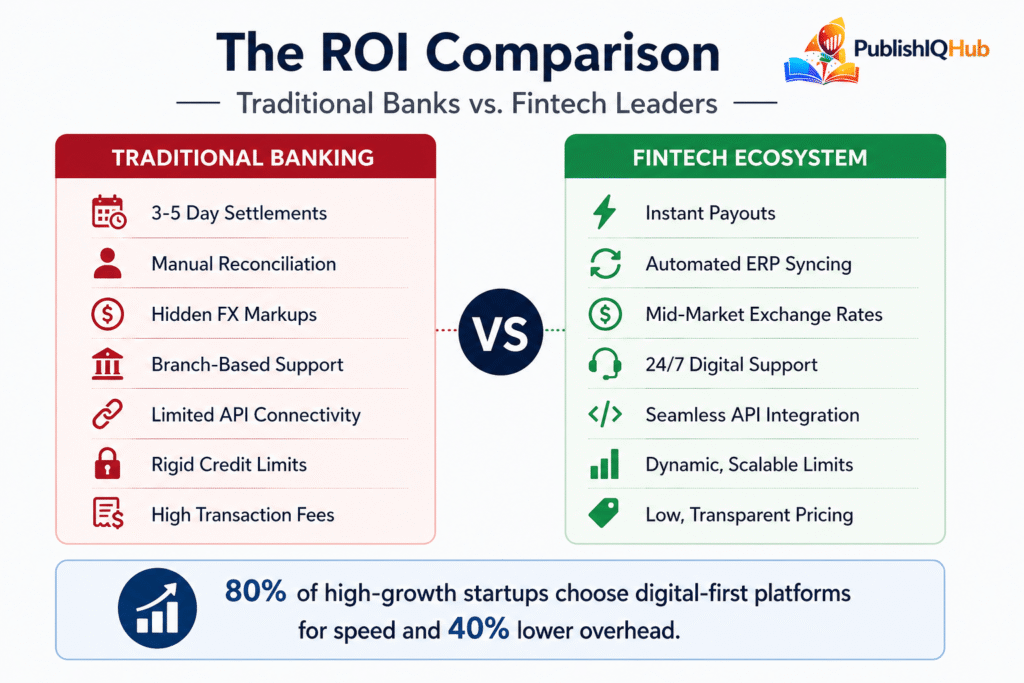

- Reduced Operational Friction and Automation: One of the biggest drains on a finance department is manual reconciliation. Modern fintech platforms automate invoice-to-payment matching. When a business uses a platform like Stripe or Adyen, the data flows directly into their accounting software. Furthermore, the ability to issue virtual cards to employees instantly enables decentralized spending without losing centralized control. This reduces the administrative workload on accounting departments by as much as 40 percent in some organizations.

- Global Market Access Without Local Infrastructure: Historically, if a company wanted to sell in fifty different countries, it needed dozens of local banking relationships. Fintech platforms have solved this by creating “global accounts.” Now, a business in India can accept Brazilian Pix payments or European SEPA transfers through a single integration. This democratization of global commerce allows even small startups to operate like multinational corporations from day one.

- Enhanced Data Security and Fraud Prevention: Because fintech leaders are technology companies first, their approach to security is proactive. They utilize advanced machine learning models that analyze behavior patterns to stop fraud before it happens. This often surpasses the security capabilities of mid-sized traditional banks that rely on older, rules-based systems. By utilizing biometric authentication and hardware-level encryption, these companies provide a level of trust that is essential for high-volume digital commerce.

The shift toward these platforms is no longer a trend but a dominant market reality. Enterprise fintech has officially overtaken the consumer segment as the primary driver of global market growth. This is most visible in the commercial sector, where digital-first commercial cards now command a 73.7 percent share of the business payment market. Large institutions are increasingly abandoning traditional corporate credit lines in favor of these fintech solutions, primarily to achieve the digital infrastructure and connectivity required for real-time global operations.

Comprehensive List of the Top 15 Fintech Companies in 2026

The following companies represent the current pinnacle of financial technology innovation. They have been selected based on their market share, technological moat, and ability to influence the wider financial ecosystem.

| Company Name | Primary Category | Best For | Competitive Edge |

| Stripe | Payments Infrastructure | SaaS and Marketplaces | Flexible, developer-first API ecosystem |

| Revolut | Consumer Super-App | International Travelers | Multi-currency accounts and global lifestyle features |

| Adyen | Unified Commerce | Enterprise Retailers | Single-platform for online and in-store payments |

| Plaid | Data Connectivity | Fintech App Developers | Secure bank linking across thousands of apps |

| Nubank | Digital Banking | LATAM Consumers | No-fee banking for underserved users |

| Klarna | Shopping and Payments | AI-Driven Retail | Integrated shopping discovery and credit tools |

| Global Transfers | Spend Management | Corporate Cost Savings | AI-driven insights to reduce unnecessary spend |

| Wise | Global Transfers | International Remittance | Transparent mid-market exchange rates |

| Mercury | Startup Banking | Tech Founders | Built specifically for venture-backed startups |

| Brex | Enterprise Spend | High-Growth Companies | High-limit cards with global expense tools |

| Razorpay | Gateway and Neobanking | Indian Digital Economy | Strong UPI and local payment ecosystem |

| Chime | Consumer Neobanking | US Daily Banking | Fee-free overdraft and early salary access |

| Block (Square) | Physical Commerce | Small Business Retail | Integrated POS hardware + software ecosystem |

| Airwallex | Global Business Accounts | Borderless SMBs | Multi-currency accounts with low transaction fees |

| Multi-currency accounts with low transaction fees | Performance Payments | High-Volume Merchants | High authorization rates for complex transactions |

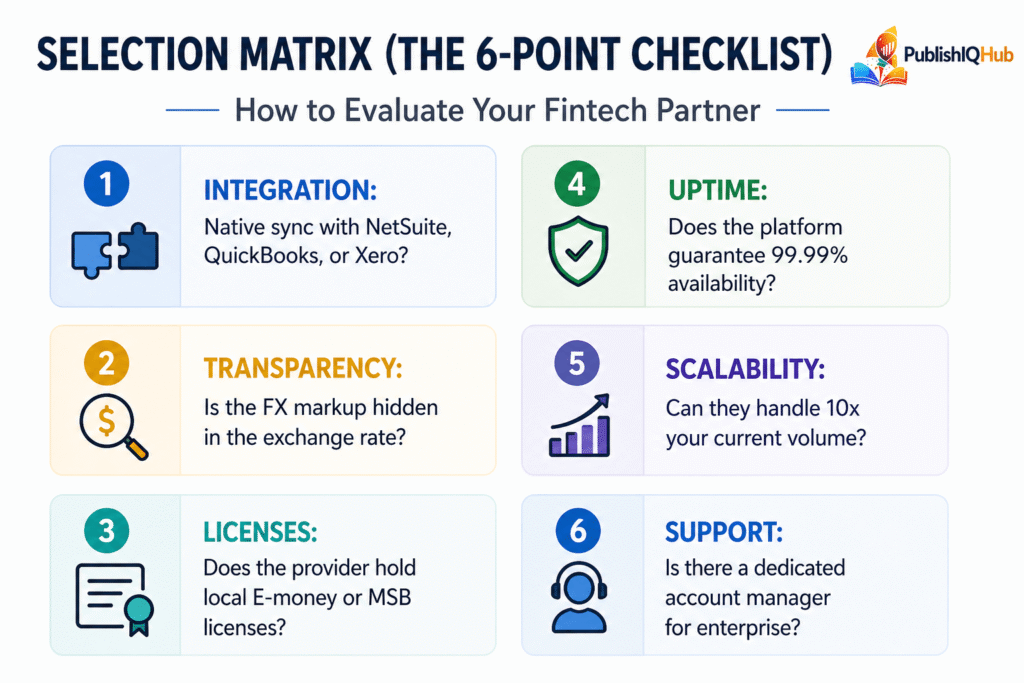

Step-by-Step Strategy for Selecting the Best Fintech Platforms

Choosing a fintech partner is a high-stakes Checkout.com decision. Unlike a marketing tool, a failure in your financial stack can lead to lost revenue and legal complications. Decision-makers should evaluate potential partners based on the following four-phase framework:

Phase 1: Integration Capability and Documentation: The first question should always be: “Does it play well with our current tech?” Does the platform have a robust, well-documented API? Does it integrate natively with your existing ERP or accounting software like NetSuite, QuickBooks, or Sage? If you have to build custom “middleware” just to get data from your payment processor to your ledger, you are creating future technical debt.

Phase 2: Fee Transparency and Total Cost of Ownership: You must look beyond the headline transaction rate. Many platforms offer a low percentage rate but hide costs in foreign exchange markups, “payout fees,” or monthly “platform maintenance fees.” Request a detailed scenario-based pricing breakdown (e.g., “What does it cost us to process 1 million dollars in cross-border transactions from five different currencies?”).

Phase 3: Regulatory Standing and Compliance Moat: Finance is the most regulated industry on earth. Ensure the provider holds the necessary licenses (like E-Money licenses in Europe or MSB registrations in the US) in every region where you operate. Furthermore, ask about their compliance automation. Do they handle the tax collection (VAT/GST) for you? Do they handle the KYC (Know Your Customer) checks? A partner that handles compliance for you is worth more than a slightly cheaper partner that leaves the legal burden on your shoulders.

Phase 4: Support at Scale and Incident Management: When a payment gateway goes down at 2:00 AM on Black Friday, a chatbot is not enough. Ensure the provider offers 24/7 priority support with a dedicated account manager for enterprise-level clients. Review their historical uptime data and their “incident report” transparency. You need a partner that is honest about their failures and fast with their fixes.

The Business Value and ROI of Implementing Top Fintech Services

The transition to modern fintech services is not just an IT upgrade; it is a strategic move that delivers measurable returns on investment. Organizations that migrate from legacy banking systems to leading fintech companies typically observe the following:

- Lower Transaction and Administrative Overhead: By utilizing digital-first platforms, companies can often reduce the per-transaction cost of international payments by 60 to 80 percent. Additionally, the automation of expense reporting and reconciliation can save an average mid-sized company over 500 manual hours per year.

- Faster Capital Velocity and Cash Flow Management: Features like “instant payouts” and real-time settlement allow businesses to access their earned revenue in hours rather than the 3-5 days typical of older systems. This improved liquidity allows for faster reinvestment into inventory or marketing, accelerating the overall growth of the business.

- Enhanced Risk Mitigation and Security ROI: Advanced fraud detection algorithms on these platforms can reduce the incidence of chargebacks and unauthorized transactions by up to 30 percent. Furthermore, by outsourcing data storage to a Tier-1 fintech provider, the business reduces its own “attack surface,” lowering the risk of a catastrophic data breach.

Emerging Trends Among the Top Fintech Startups

While the leaders continue to grow, a new wave of top fintech startups is addressing specific gaps in the market. These companies are worth watching for their specialized focus and potential for disruption:

- Embedded Finance and Banking-as-a-Service (BaaS): We are seeing the rise of startups that allow non-financial brands (like a car company or a retail chain) to offer credit or insurance at the point of sale. This “invisibly” integrates finance into the customer’s daily journey.

- Identity, Deepfake Detection, and Fraud Prevention: As AI makes it easier to create fraudulent identities, a new niche of fintech startups is focusing solely on the security layer. They use behavioral biometrics, like how a person types or moves their mouse, to verify that the user is a real human and not a bot or a stolen identity.

- Real-World Asset (RWA) Tokenization: There is a growing movement toward digitizing physical assets like real estate, gold, or art. Platforms in this space are using blockchain technology to fractionalize these assets, making them as liquid and easy to trade as a share of stock.

Future Outlook: The Next Frontier for Global Fintech Growth (2026-2030)

As we look toward the end of the decade, the fintech industry is entering a phase of hyper-maturity. The global fintech market size is projected to increase by over 1,000 billion dollars by 2030, growing at a compound annual growth rate of approximately 32 percent. This expansion is no longer driven by the simple digitization of banking but by the creation of entirely new financial ecosystems that operate autonomously across borders.

- Rise of RegTech:

One of the most significant shifts occurring in 2026 is the rise of RegTech (Regulatory Technology) as a strategic pillar. For years, compliance was viewed as a cost center: a necessary hurdle that slowed down innovation. However, leading fintech companies are now turning compliance into a competitive advantage. By using AI to automate real-time risk assessments and anti-money laundering (AML) checks, these platforms can onboard enterprise clients in minutes rather than weeks. This shift is particularly vital as regulators in the EU, US, and APAC introduce stricter frameworks around data privacy and digital asset transparency.

- The Decentralization of Global Settlement Rails:

Another massive trend shaping the future is the modernization of global settlement rails. Traditional cross-border payments have long relied on the SWIFT network, which can be slow and expensive due to the multiple intermediary banks involved. In response, we are seeing the emergence of high-speed, blockchain-based settlement networks that allow for near-instant movement of capital.

Top fintech companies like Airwallex and Wise are already leveraging these technologies to provide “local” payment experiences globally. In the next few years, the integration of Central Bank Digital Currencies (CBDCs) and tokenized real-world assets will further bridge the gap between traditional finance and the digital economy. This will allow businesses to treat global liquidity as a single pool, moving money between a New York headquarters and a Singaporean subsidiary with the same ease as a domestic transfer.

- Hyper-Personalization and the Invisible Finance Era:

We are also moving into the era of “Invisible Finance.” This is a state where financial services are so deeply embedded into our daily software that we no longer think of them as separate tasks. Whether it is a SaaS platform providing instant working capital loans based on your invoice history or an e-commerce site offering automated insurance at the point of sale, finance is becoming a contextual service.

This “embedded everything” model relies heavily on data integrity. As financial platforms ingest more data points, from supply chain logistics to social media engagement, they can build hyper-personalized risk profiles. This allows for “Segment of One” banking, where interest rates, credit limits, and investment strategies are tailored specifically to the real-time needs and performance of a single business or individual.

Strategic Comparison: Market Segments of the Leading Fintech Companies

To help you navigate this crowded market, we have categorized the top 15 fintech companies based on their primary market impact and technological focus.

Category 1: Infrastructure and Payment Gateways

Companies: Stripe, Adyen,Checkout.com, Razorpay

Role: These companies act as the “plumbing” of the internet. They focus on high uptime, developer flexibility, and maximizing transaction authorization rates. They are essential for any business selling products or services online.

Category 2: Data Aggregators and Open Banking

Companies: Plaid

Role: These firms do not move money themselves; they move the data that makes moving money possible. They provide the secure “handshake” between your bank account and your favorite apps.

Category 3: Business Spend and Financial Operations

Companies: Ramp, Brex, Mercury, Airwallex

Role: These platforms are designed for the CFO and the finance team. They replace traditional corporate cards and manual expense reports with automated, software-driven spend management.

Category 4: Consumer-First Neobanks and Super-Apps

Companies: Revolut, Nubank, Chime, Block (Square)

Role: These companies focus on the end-user experience. They aim to be the “primary financial home” for individuals, offering everything from no-fee checking accounts to stock and crypto trading.

Category 5: International Transfer Specialists

Companies: Wise

Role: These firms focus on the specific pain point of currency exchange. By bypassing traditional banking networks, they offer lower fees and more transparent rates for global remittances.

Conclusion: Securing Your Position in the Future of Finance

The fintech industry today is defined by efficiency, transparency, and accessibility. The companies listed in this guide have proven that they can handle the scale and security required by the modern world. Whether you are a consumer looking for a better way to manage your personal wealth or an enterprise seeking to optimize a global supply chain, these platforms provide the foundation for success.

By staying informed on the leading fintech companies and the rising top fintech startups, you can build a financial stack that is not only efficient today but also resilient for the challenges of tomorrow. The future of finance is not a bank building; it is a secure, global, and instantaneous network.

Frequently Asked Questions

What exactly makes a company a fintech?

Fintech, short for financial technology, refers to any company that uses software and modern technology to provide financial services. This can range from mobile banking apps and payment processors to digital lending, insurance (insurtech), and investment platforms.

Are top fintech startups as safe as traditional banks?

While most fintech companies are not banks themselves, they partner with regulated, traditional banks to hold user funds. This means your money is often protected by government-backed insurance (like FDIC in the US or FSCS in the UK). The fintech company provides the innovative interface, while the partner bank provides the regulated vault.

How do I know if a fintech company is right for my small business?

Start by identifying your biggest pain point. If you sell mostly online and struggle with checkout conversion, a payment processor like Stripe is essential. If you have a team with messy expenses, a spend management tool like Ramp or Brex is the right choice. If you are a freelancer working with global clients, Wise Business is likely your best starting point.

Why is data hygiene so important for fintech platforms?

Financial systems rely on accurate data for everything from credit scoring to fraud detection. If a database is cluttered with duplicate records or incorrect address information, the financial platform’s algorithms cannot perform effectively. This can lead to declined transactions, higher fraud risk, and lost revenue.

What is open banking, and why does everyone talk about it?

Open banking is a regulatory practice that mandates banks to allow third-party financial service providers (like Plaid) to access consumer financial data through secure APIs, with the consumer’s permission. This allows you to connect your bank account to various apps for better budgeting, faster loan approvals, and more personalized financial advice.

Does fintech improve financial inclusion for the unbanked?

Yes. By using alternative data, such as utility bill payments, rent history, and mobile phone usage, fintech companies can provide credit and banking services to millions of people who lack a traditional credit score. This is particularly transformative in emerging markets in Africa, Southeast Asia, and Latin America.

What are “Gas Fees” in some fintech and crypto apps?

Gas fees refer to the transaction fees paid to miners or validators on a blockchain network to process a transaction. While many traditional fintechs hide these costs or pay them for you, crypto-focused fintechs often pass these costs directly to the user.